The slow zombie crawl of housing inventory eased last week as inventory turned negative week-over-week. In addition, mortgage rates rose to their highest in a year as labor data held steady and purchasing apps had their first negative week after three consecutive weeks of positive growth.

Thank you for reading this post, don't forget to subscribe!- Weekly Active Inventory declined 866 houses

- Mortgage rates hit year-on-year highs 7.22%

- Shopping apps declined 5% week over week

weekly housing list

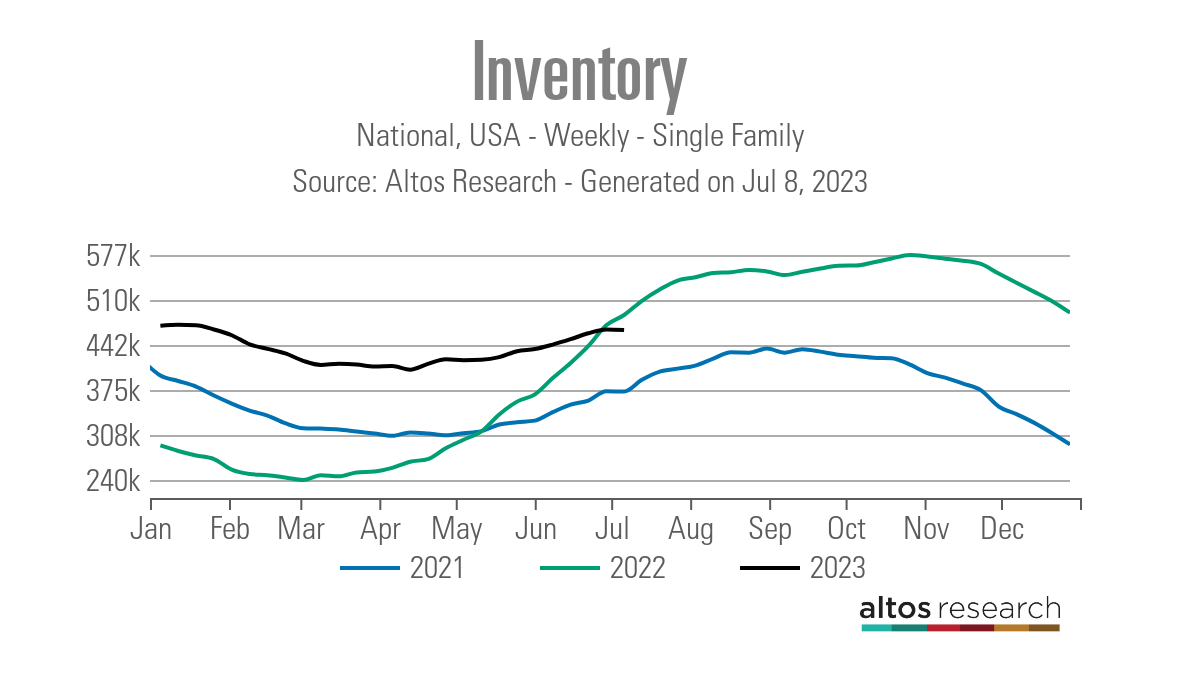

We scored a hat trick on housing last week: Weekly active listings were negative week-over-week, new listings were negative week-over-week, and active listings + new listings data is negative year-over-year. It’s actually a very unhealthy housing market because we have too many people chasing too few houses.

There was a rare week-over-week decline in weekly active listings data. Part of this can be attributed to the 4th of July holiday, but this year’s trend is so different from last year that it’s not 100% based on the holiday week.

- Weekly inventory change (June 30-July 7): Inventory declined 465,755 To 464,889

- Same week last year (July 1-July 8): Inventory increased 472,046 To 487,319

- Inventory was the bottom for 2022 240,194

- Inventory peak so far for 2023 472,688

- For reference, active lists for this week 2015 Were 1,197,641

Housing inventory growth has been so slow this year that active listings data today in July haven’t even exceeded our January levels, which is usually when we see a seasonal low for the first half of the year. As we can see in the chart below, it’s slowing so much that year-to-date inventory is now negative as of 2022.

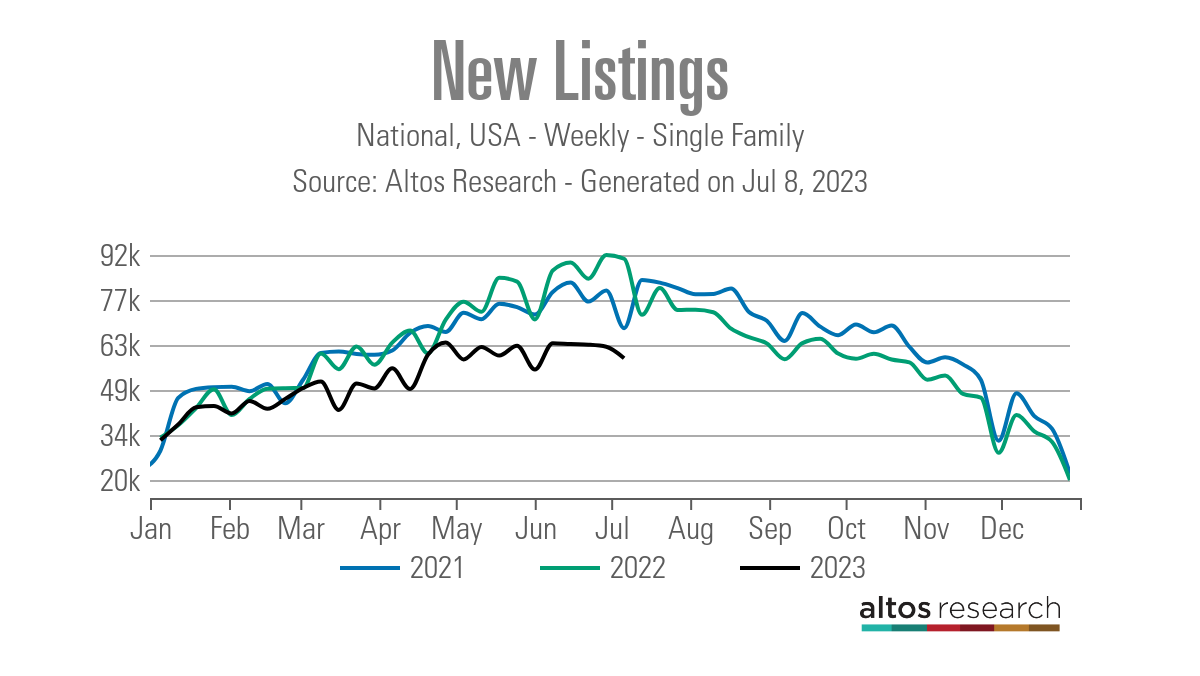

The other big story in the housing sector is that new listing data is trending at the lowest level recorded in 12-month history. We have had four consecutive weeks of downtrends and we are about to encounter a seasonal downtrend in this data line. As we can see below, there is a big difference between this week’s 2023 data vs 2022 data.

- 2023: 58,813

- 2022: 90,336

- 2021: 68,328

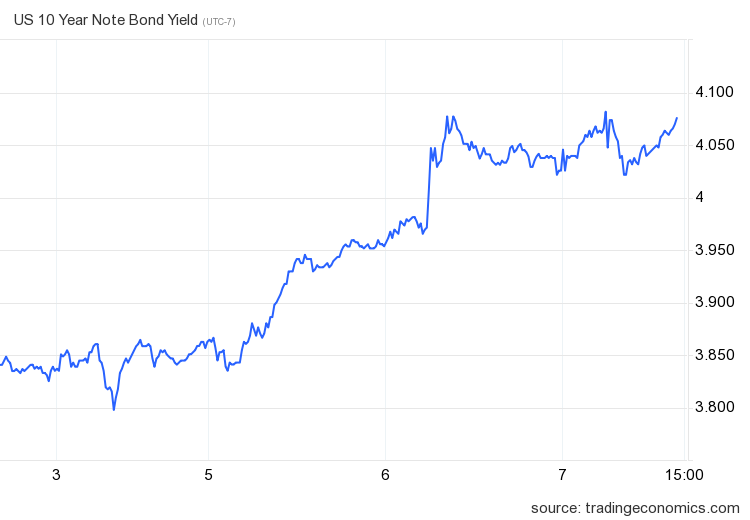

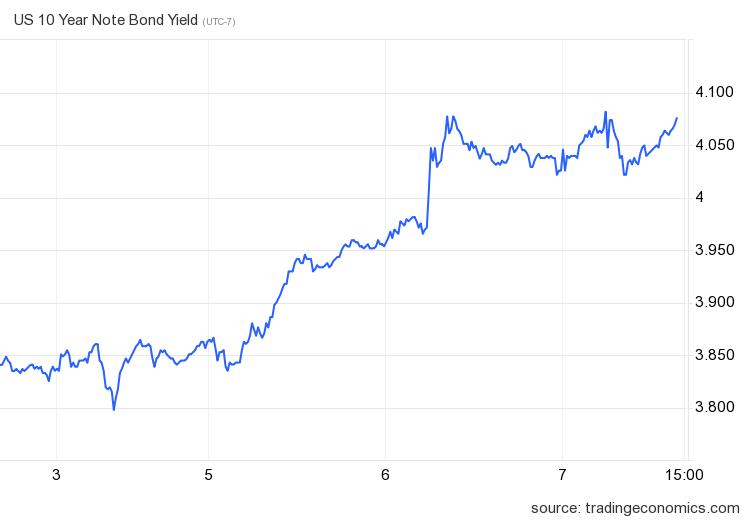

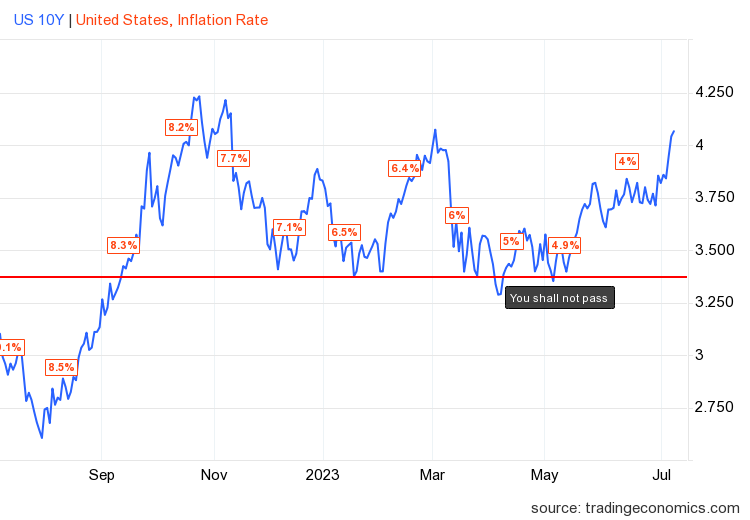

10-Year Yield and Mortgage Rates

Mortgage rates started the week at 7.03% and ended at 7.14%. The 10-year yield is near a yearly high as the US bond market doesn’t see a job recession anytime soon. As you can see below, bond yields increased significantly during the jobs week.

In my 2023 forecast, I said: If the economy remains stable, the 10-year yield range should be between 3.21% and 4.25%, which equates to mortgage rates between 5.75% and 7.25%. The labor market remains healthy as long as unemployment claims remain below 323,000 at the four-week moving average. As we can see below, the 10-year yield has been in this channel 100% of the time in 2023, but mortgage rates are on the verge of breaking above 7.25%.

As the gap between the 10-year yield and mortgage rates has worsened since the banking crisis, this puts upward pressure on rates to exceed my estimate in 2023. The chart below shows the increasing spread since the start of the SVB banking crisis. ,

![]()

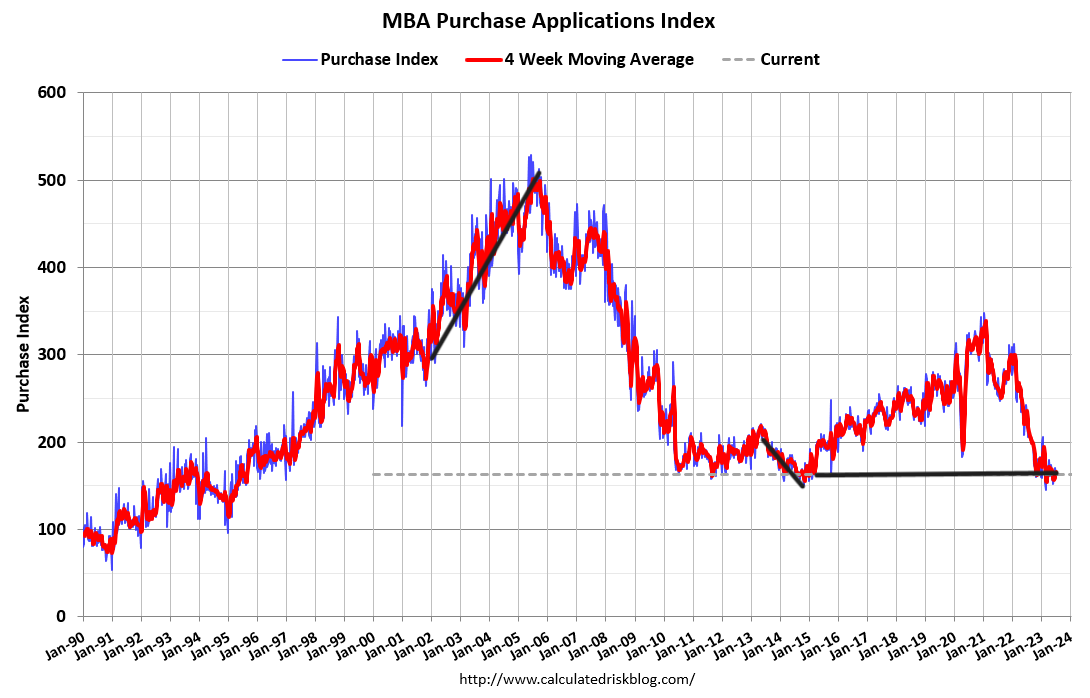

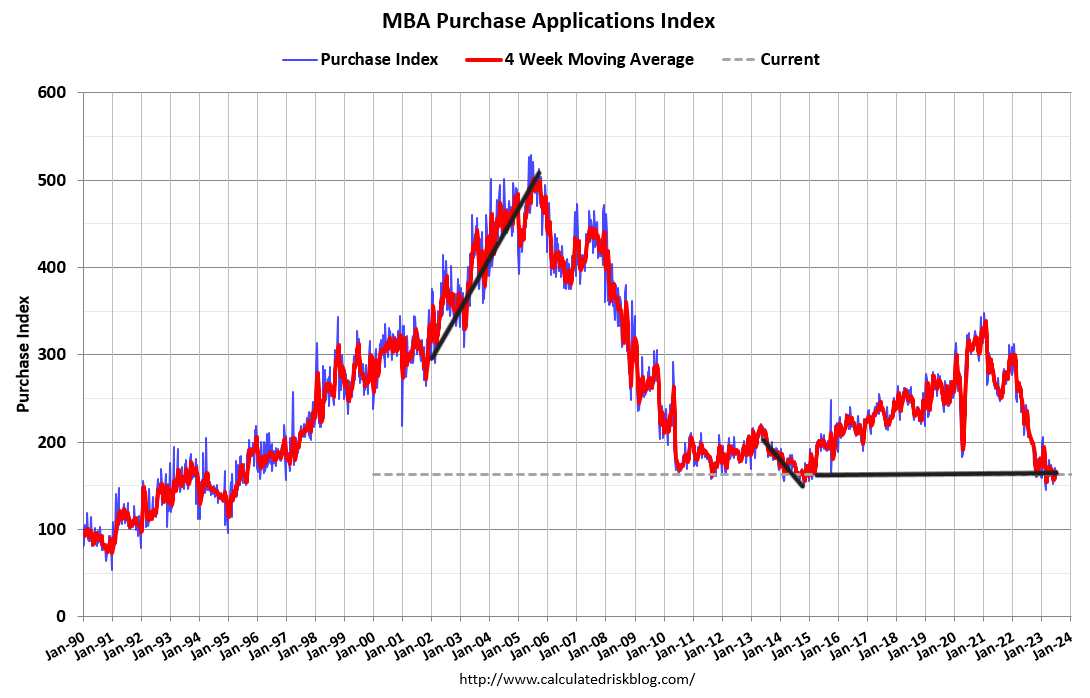

buy app data

Shopping app data declined 5% weekly, counting year-to-date data 13 positive And 12 negative print. If we start on November 9th, 2022, it’s done 20 positive print vs 12 negative print. Given that mortgage rates have been around 7% and above over the past month, three of the past four weeks being positive shows that the 2022 collapsing market has turned around after Nov. 9.

But remember: The bar with shopping apps is so low that we can exceed it. While we know Data has stabilized from the waterfall dive, we’re all in the same boat with Data this year.

Next week: Inflation Week!

Inflation week is here again, and we have two inflation reports to work with. Between the key CPI data and the PPI data, we should see the same story: Headline inflation data is clearly falling, but core inflation data is a bit more sticky. Nevertheless, with the fall in used car prices over the next few months, the sheltering aspect of inflation will be more dominant here. Below are the year-by-year core CPI data.

Considering where we are with 10-year yields and mortgage rates, the expectedly lighter CPI inflation print this week will be just what the housing market needs to drive mortgage rates lower.