The financial press is again buzzing about the deadline for the debt ceiling and the risk of another government shutdown and perhaps a catastrophic default on the US debt if no deal is reached. terrace (currently sitting $31.4 trillion) is set to hit the theaters on June 1.

Washington Post is specifically apoplectic,

“Federal workers took leave. Social Security checks have been put on hold for senior citizens. Rising mortgage rates. A global financial system sent again …

“Leaders in Congress and the White House are trying to strike a deal to raise the federal debt limit, with only weeks to go before the Treasury Department may no longer be able to avert an unprecedented US default. If they fail, and the government is unable to meet its payment obligations, economists and financial experts predict chaos.

“It would be a deadly combination,” said Mark Zandi, Moody’s chief economist. ‘You can see how this thing could really metastasize and take down the entire financial system, which would eventually wipe out the economy.’

Well, that sounds rather bad. So, is this something real estate investors should be worried about, and if so, how should one prepare?

Let’s first start with a quick overview of what is going on and how such “fiscal crises” have gone down in the past.

Recent History of the Debt Ceiling Debates

The debt ceiling is believed to set a limit on the total amount that the United States federal government is authorized to borrow. In recent years, for the most part, this “ceiling” has been a joke.

As the website for the US Treasury Department notes“Since 1960, Congress has acted 78 different times to permanently raise, temporarily raise or modify the definition of the debt ceiling.”

I’m not sure what you call something that has been raised more than once a year for over half a century, but a “ceiling” doesn’t seem like quite the right word for it.

However, talks break down midway, and zero rings out before an agreement to raise the debt limit or reduce spending (or a combination of both) can be reached. In such cases, a “government shutdown” applies. However, it should be noted that such shutdowns are only partial and usually involve giving leave to government employees and suspending entitlement payments, etc.

been there 10 government shutdowns since 1980, although all four that occurred in the 80s lasted less than a day (two for only about four hours). The longest that happened before the turn of the century was in 1995 and 1996 and lasted 21 days. Only a few agencies were affected and about 284,000 federal employees were sent on furlough. (This came shortly after 800,000 people were furloughed in a five-day shutdown a month earlier.)

Since the Great Recession and subsequent ballooning of the federal debt, political wrangling over the debt ceiling has intensified. Since then, there have been two nasty debt ceiling fights that resulted in shutdowns. The worst was probably in 2013, which led to a 16-day shutdown that affected all agencies and sent 800,000 federal workers on furlough.

A bipartisan “super committee” was supposed to cut $1.5 trillion over the next 10 years, but failed to do so. Thus, we missed out on a whole board (except for rights) budget seizure That basically nobody was happy.

The cuts reduced spending by about $1.1 trillion over the next eight years from what they would have been otherwise. (Though some of that sequencer was later removed).

In January 2018, there was the longest shutdown on record—35 days—mainly due to disagreements Regarding the proposed border wall, The cost to the government was estimated at $5 billion.

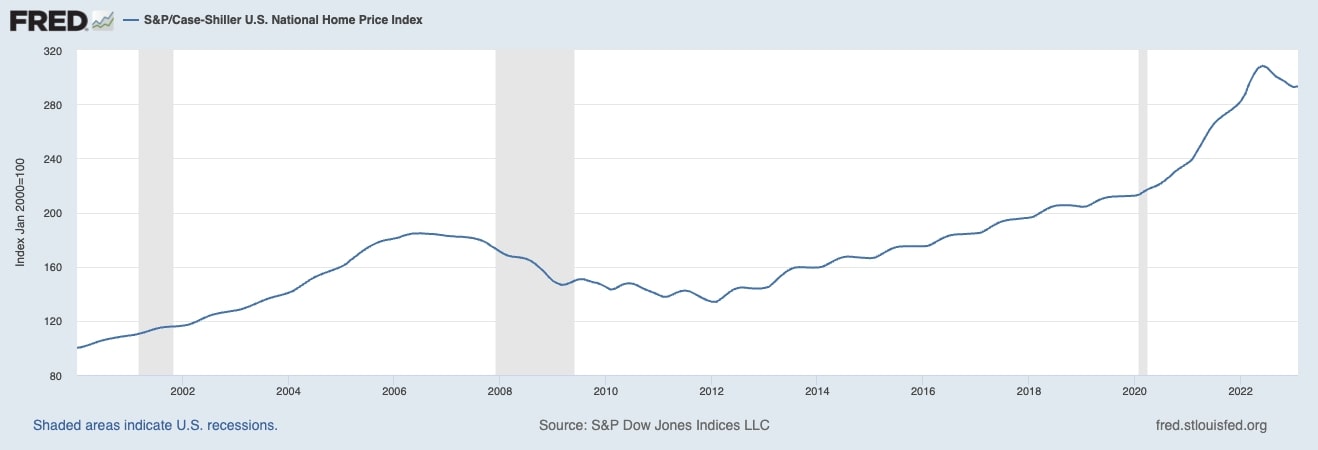

That’s not a big change, and there was a lot of disruption from these shutdowns. For example, air travel was put under pressure, national parks were closed, and a host of other problems and inconveniences occurred. But there was no significant effect. And it went without notice to real estate investors No effect on prices Neither by any shutdown nor by confiscation.

If the budget deficit was ruffling a few feathers in 2013, said rustle has multiplied as the US budget deficit passed $1.1 trillion For the first half of the financial year 2023. And it doesn’t seem to justify such expenditure anymore after the Covid-19 pandemic hit.

US Deficit Tracker – Bipartisan Policy Center

Of course, just because the budget is out of whack doesn’t explain how to address such an imbalance. what cuts How much? Should taxes be raised? Which and by what amount? Obviously, there’s a lot to argue about.

here on the issue variety of issues, unspent COVID-19 funds (about $30 billion), future budget caps, regulations on energy development, and work requirements for those receiving food stamps, Medicaid and/or TANF (Temporary Assistance for Needy Families) Including whether to increase or not. In other words, there are too many things to discuss at the table.

With so much on the table, getting a deal can be difficult. Thus, the deadline may have passed, which is what the fuss is all about. If the deadline is missed, Treasury will continue to pay Despite being closed until it runs out of money. If it expires without some sort of resolution, the US federal government will (or at least officially, some argue) default on its debt for the first time in its history. has effectively missed in the past,

And while a shutdown wouldn’t be particularly bad, a default would be catastrophic.

Should we worry about potential defaults?

the last article i wrote was on mortification and the importance of not letting the things you can’t control affect your well-being. And assuming you’re not a member of Congress, it’s certainly one of those things you can’t control.

But going forward, the chances of an outright default are extremely slim. I don’t have a lot of faith in politicians, but the sheer insanity of failing to pay down our debt when the money was available to do so would be inconceivable.

It needs to be remembered that this is not an either/or issue. The government will either not come to an agreement or fail. There are a number of temporary and temporary measures that can (rather easily) be done to avoid a default, even if they don’t avoid a shutdown. This would include passing a temporary extension on the debt ceiling deadline, which has already been done.

If any default happens, it will cause very serious problems for the real estate investors. American banks will be under pressure and credit will run out. Therefore, it will be almost impossible to get a bank loan. Yahoo! predicts that mortgage payments will go up a good 22%, Credit lines will probably be called, so investors will lose access to them. Thus, there is a possibility of a fall in the prices of real estate. The economy would be hit by a recession, and many tenants would lose their jobs, leading to an increase in crime. Contractors and vendors will go out of business, making it difficult to find people to do the work, even if you have the money to pay.

As far as preparation goes, well, if you haven’t already built your underground bunker and stocked up on a year’s supply of food, at this point you can invest any money you have in the stock market. Can’t do much except take it out.

In short, this would be very bad for real estate investors, and having my predictions from this article thrown in my face would be the least of my problems.

That being said, this is not going to happen. Ultimately, to get there we have to go through these steps:

- There can be no deal till June 1.

- No deal can be done before the Treasury runs out of money to make interest payments.

- No extension or temporary deal is done for payment of interest payment.

- Once the payment is missed, financial markets start to panic, Congress doesn’t immediately change course and pay down its debt.

I’d say the difference between 1) and 2) is at least possible, though not likely. 3) is fundamentally impossible, and 4) downright unfathomable.

And all of this assuming the Biden administration doesn’t pull an end race around congress Through some legal shenanigans, which they could potentially do if the loan term expires and default looms.

Yes, it’s never wise to bet your money on the intelligence of politicians, but I expect them to breathe and eat and sleep deliberately, and avoid defaulting when there is money to pay, no more than the previously stated expectations. Is asking for

conclusion

MSCI puts up odds of default % on twoWith its head of portfolio management research, Andy Sparks, saying the likelihood is “small, but it’s not zero.”

Kind of reminds me of this meme.

Yes, the prospect of a possible default makes big headlines, but it is exceptionally unlikely.

But other than that, there is little the average person can do to affect it, and it is too late to make any sweeping adjustments in such a dire scenario.

In general, though, we’re sailing through choppy economic waters, even if a government default is not in the cards. As i wrote earlier,

,[The] The best investors often do best during recessions or unstable economies. However, they do not do this by sitting on the sidelines. Instead, they keep their [cash] Reserve high, adjust with the environment, sharpen your pencil, and continue…”

There will be financial problems ahead. Be cautious and conservative, but don’t stop and buckle down just because of some doomsday headlines.

Close more deals in less time for less money

money without cash Will fully prepare you to find off-market leads, uncover sellers’ motivations, negotiate with confidence, close more deals, build a team and much, much more. This book by Pace Morbi has everything you need to become a millionaire investor without using any of your own capital.

Note by BigPockets: These are the views expressed by the author and do not necessarily represent the views of BigPockets.