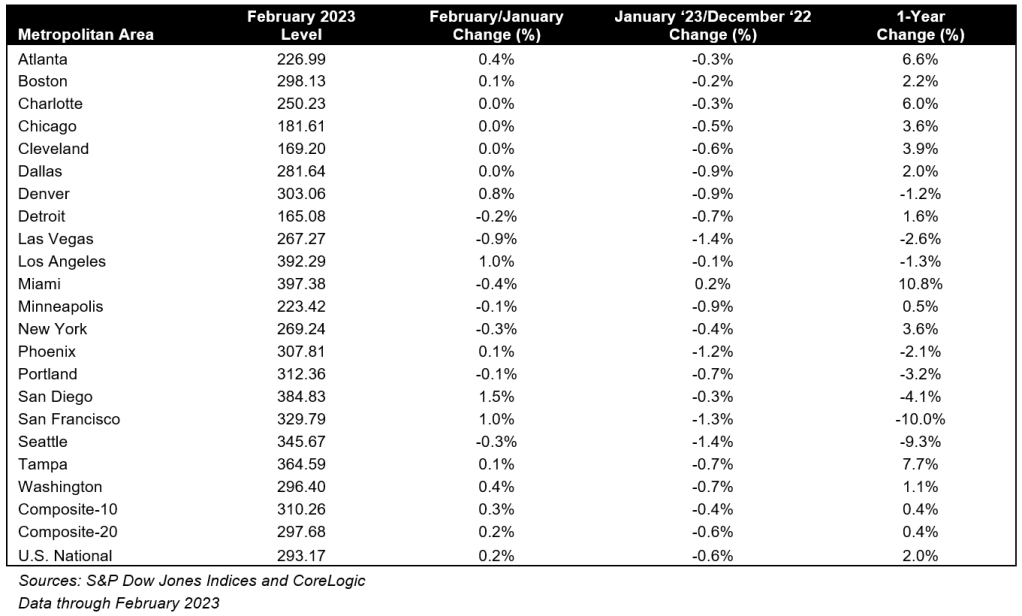

Home price growth cooled further in February, falling to an annual rate of growth of 2.0% S&P CoreLogic Case-Shiller National Home Price Index, released on Tuesday. The annual growth rate in January was 3.7%.

Thank you for reading this post, don't forget to subscribe!The national index came in at a reading of 293.17 in February. On a month-to-month basis, the index was up 0.2% before seasonal adjustments.

“The home price trend in February 2023 is bearish,” Craig Lazzara, managing director of S&P DJI, said in a statement. “The National Composite, which had fallen for seven straight months, rose a modest 0.2% in February, and is now down 4.9% from its June 2022 peak.”

The February figures precede challenges in the commercial banking industry that began in early March, however, with industry forecasters predicting interest rates will remain high as federal Reserve Continued to focus on its inflation-reduction goals.

“Mortgage financing and economic weakness are likely to remain a headwind for housing prices for at least the next several months,” Lazzara said.

However, despite recent increases, continued low inventory conditions are expected to hold up home prices nationally.

“Inventory remains low as sellers lock in their low mortgage rates, even as affordability barriers amid volatile mortgage rates have turned many home buyers away from this market,” said Nicole Bachaud, Zillowsenior economist said in a statement. “Despite slower than normal demand, the low inventory environment is creating more competition on fewer homes, keeping prices down from last year’s peak, which is likely to continue in the coming months. To stay in the market and remain competitive, many buyers are looking to preserve lower priced homes, with the lowest priced homes seeing the most competition and price increases starting this spring.

The Case-Shiller Home Price Index for February is a three-month average of closing prices in December, January and February. Because most home sales take several months from contract to closing, the data is likely to include some deals that occurred in October and November.

Home price growth also slowed in February in the 20-City Composite Index, which posted an annual increase of 0.4% to a reading of 297.68. In January, the 20-cities index registered an annual growth of 2.6%. Compared to a month ago, the 20-cities index registered a 0.2% increase before seasonal adjustment.

The S&P CoreLogic Case-Shiller 20-City Composite Home Price Index is a price-weighted average of 20 metro area indexes. The base value of the indices is 100 in January 2000; In other words, a current index value of 150 translates to a 50% appreciation rate since January 2000 for a typical home located within a particular market.

The 10-City Home Price Index also posted a 0.4% annual increase, down from 2.5% in January, bringing it to a reading of 310.26. Month over month, the 10-city index rose 0.3% before seasonal adjustments.

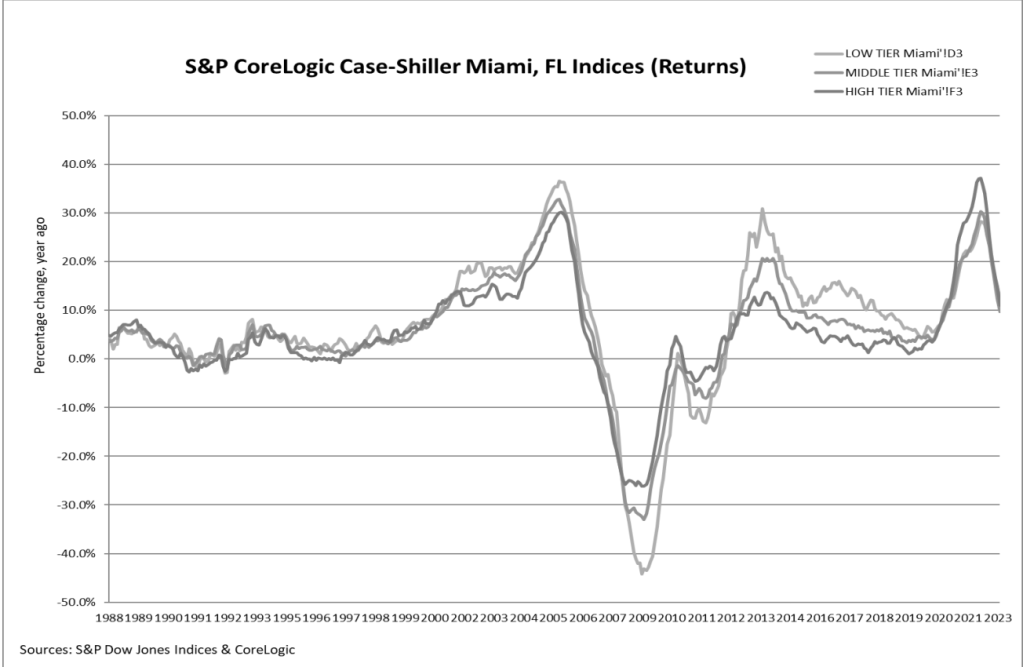

Nevertheless, Miami (10.8%), Tampa (7.7%) and Atlanta (6.6%) again reported the highest annual price gains among the 20 cities analyzed. All 20 cities recorded lower prices in the year ending February 2023 as compared to the year ending January 2023, but on a month-on-month basis 12 of the 20 cities recorded a price increase compared to only one in January .

At the other end of the spectrum, San Francisco (-10.0%), Seattle (-9.3%), and Portland (-4.1%) posted the largest annual declines among the 20 cities. Phoenix, as the star of the Case Shiller Index, posted a 2.1% annualized price decrease in February.

The February results were most interesting because of their regional differences. Miami’s 10.8% year-over-year gain made it the best-performing city for the seventh consecutive month. Tampa (+7.7%) and Atlanta (+6.6%) ) continued to rank second and third, while Charlotte (+6.0%) trailed behind. Results differed in the Pacific and Mountain time zones,” Lazzara said. “Last month, four West Coast cities (San Francisco, Seattle, San Diego and Portland) were in year-to-date negative territory. In February they were joined by four of their western neighbors, such as Las Vegas (-2.6%), Phoenix (-2.1%), Los Angeles (-1.3%), and Denver (-1.2%) all fell into negative territory. It is not surprising that the Southeast (+7.8%) remains the strongest region of the country, while The West (-4.2%) remains the weakest.