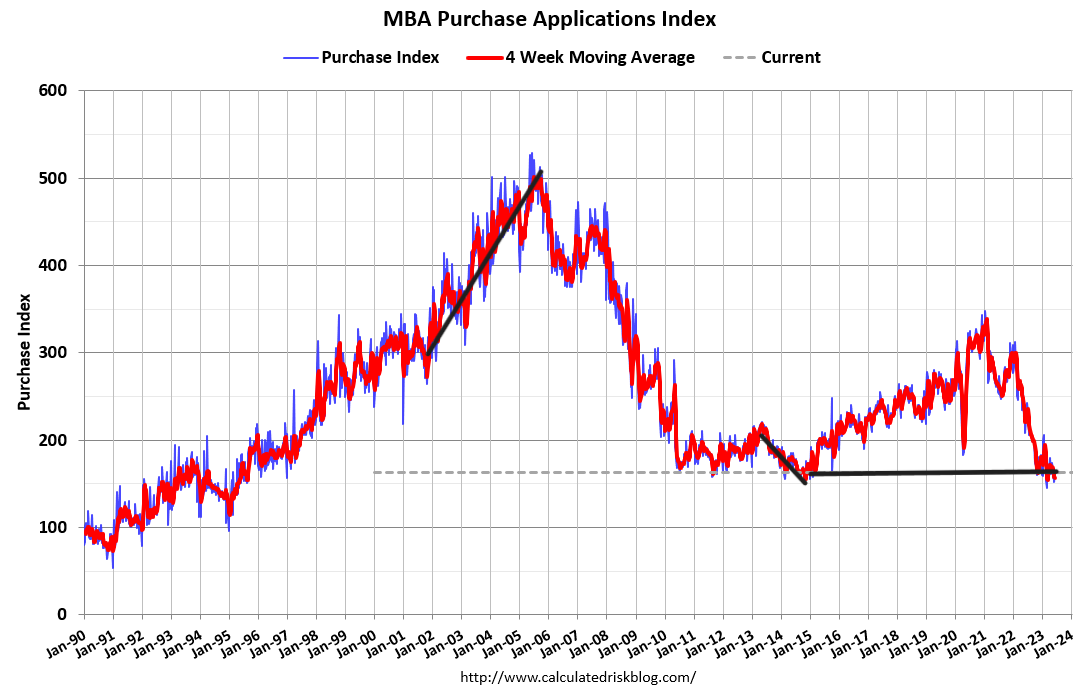

Mortgage rates were near 7% last week but purchase applications were still able to extract 8% week-over-week gains. It was surprisingly strong, but as I’ve always stressed, context is key. Purchase apps were coming off a four-week losing streak and even though the decline was week-over-week, it was still four weeks of weakness. Recent growth broke that streak, but demand is still low.

Thank you for reading this post, don't forget to subscribe!Active housing inventory increased while new listings data declined. Mortgage rates hardly budged last week, even federal Reserveannounced it was withholding rate hikes and CPI inflation reports.

Here’s a quick recap of the past week:

- active inventory increased 8,041 weekly. I’m still expecting a few weeks that show inventory growth between 11,000-16,000

- mortgage rates remained in a tight range between 6.94% -6.98%

- Purchase application data showed 8% growth week over week

buy app data

Last week’s 8% week-over-week increase was stronger than expected, with rates closer to 7%. But, last year we had the largest ever decline in Purchase App data for a year, and through November 9, 2022, this data has been forming a bottom-end range.

This dynamic changed the housing market from one where home sales were crashing to one that has now stabilized. I explain how it’s done in this recent podcast. As you can see in the chart below, the collapse in purchase application data has stalled, and if it weren’t for that, we’d be having a different conversation about the housing market today.

November 9 is an important date as the housing market trend changed at that time. Since that date, the purchase application data, after making some holiday adjustments, has printed 18 positives and 11 negatives. Year-to-date, we have 11 positive and 11 negative prints.

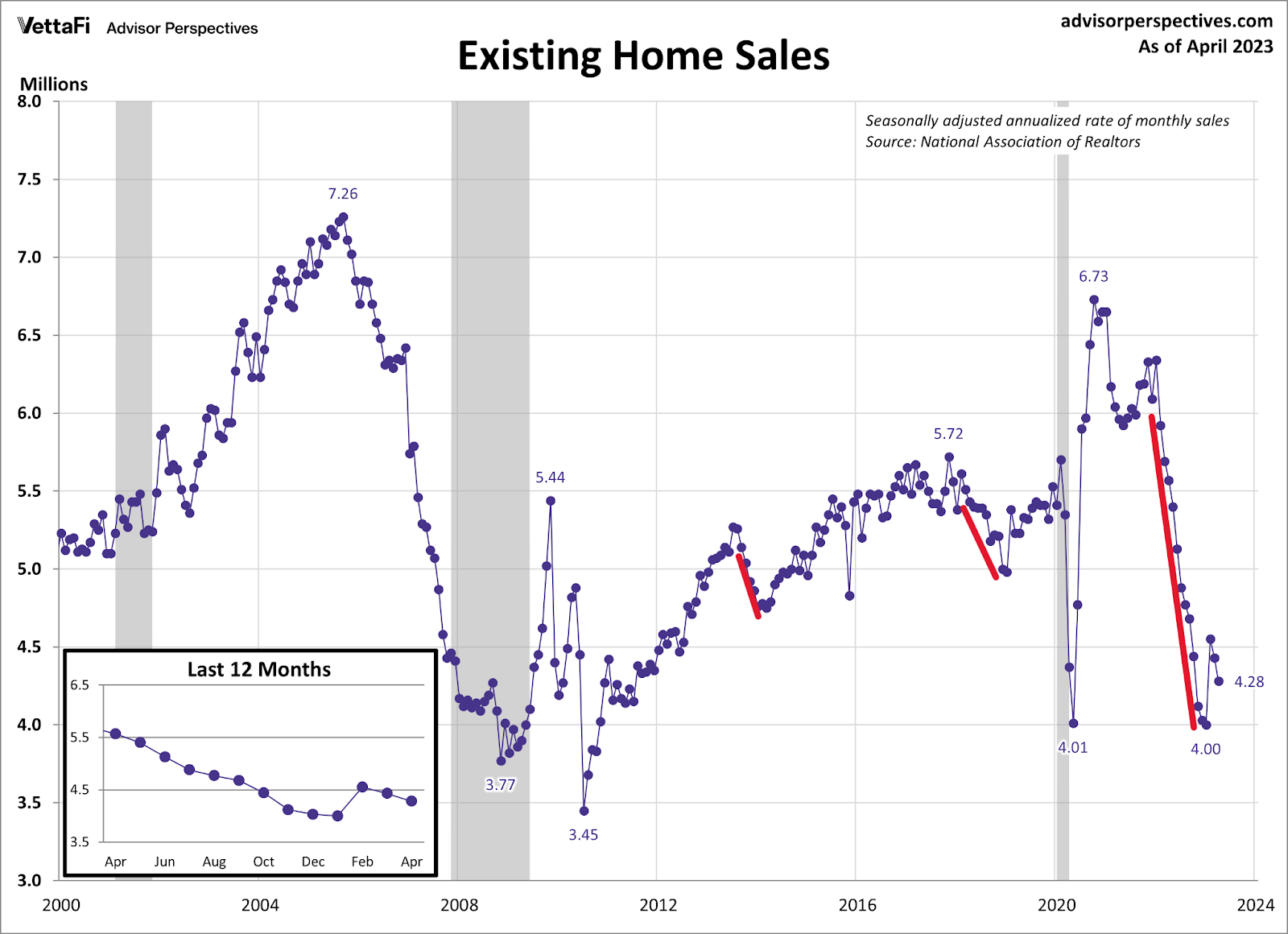

The increase we saw from November 9 through February was long enough to give us the only big current home sales print this year. Really, not much is happening after that, so sales should remain in the range of 4 million to 4.6 million this year. However, if we find more weakness in shopping apps, it is likely that this data line will go below 4 million.

Sales of existing homes are coming in, but I don’t expect any major surprises in this week’s report. We can’t break over 4.6 million this year unless we get a long string of positive purchase application data, which will require lower mortgage rates. Last year, when mortgage rates fell from 7.37% to 5.99% for a few months, we had a string of positive purchase application data that facilitated that big home sales print. Imagine what the housing market would look like if rates stayed between 5.5%-6% for a year.

weekly housing list

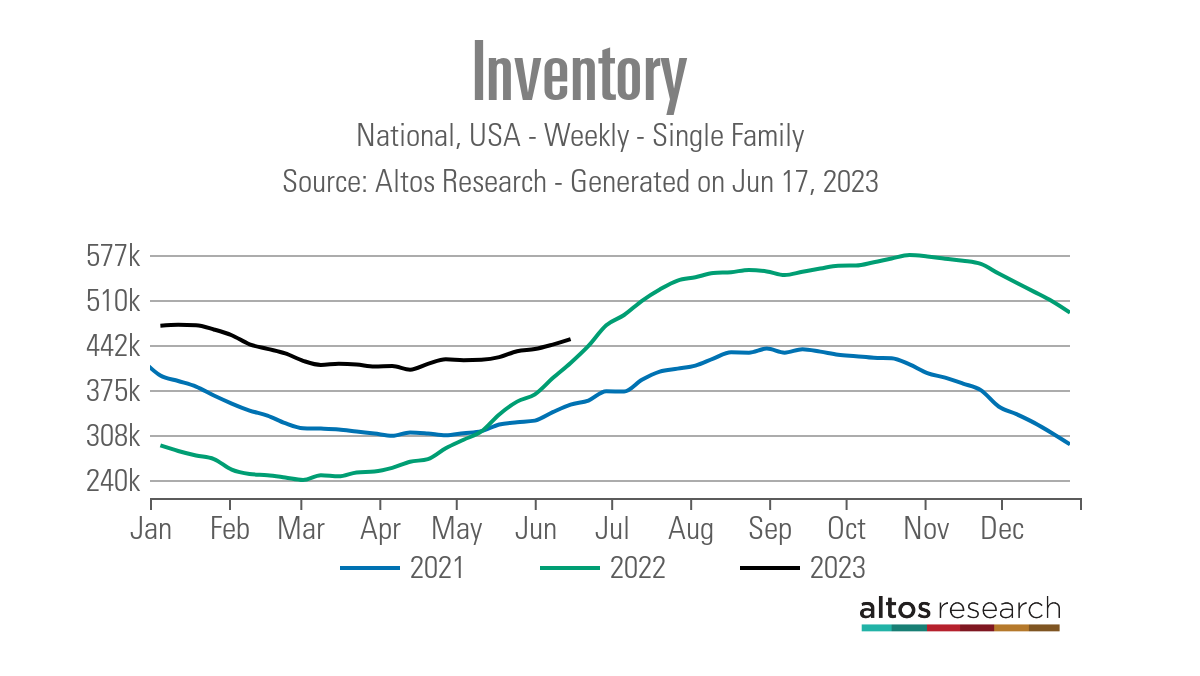

This year’s Housing Inventory theme has been The Walking Dead musical chorus of a zombie trying to escape a grave. Slow and steady and late! It took the longest time ever recorded in US history to find the seasonal inventory bottom that occurred on April 14, and has been on a slow rise since then.

But, it’s still an increase! A typical housing market always has an increase in spring inventory and then a decline in inventory in the fall and winter. While I wanted to see more inventory growth this year, I’ll do what I can.

- Weekly Inventory Change (June 9-16): Inventory to Rose 443,006 To 451,047

- Same week last year (June 10-17): Inventories increased from 392,792 To 415,582

- inventory bottom for 2022 240,194

- 2023 is the peak so far 472,680

- For reference, in the active listings for this week 2015 Were 1,173,793

As you can see in the chart below, inventory growth has been so slow that we are on the verge of showing some negative inventory data year-over-year. This occurs when procurement application data remains flat year-over-year. Of course, if we find some weakness in demand, days on market may increase and allow inventory to accumulate.

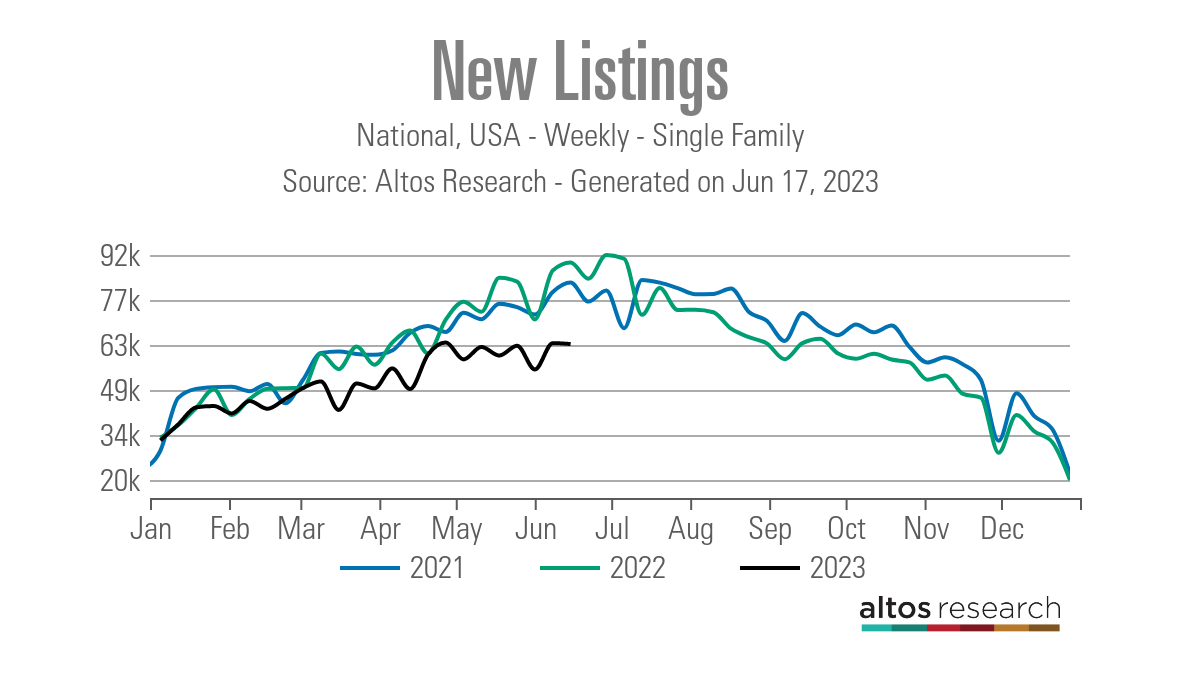

New listing data is another big story with housing inventory. Since the second half of 2022, it has been trending at all-time lows. This trend has continued throughout the year, so we have limited new housing to work with.

Below are some numbers to compare to new listing data in recent years. As you can see, last year we were showing some year-over-year growth, but not so much this year.

- 2023: 63,293

- 2022: 89,166

- 2021: 82,815

We only have a few weeks left before we see the traditional new listing data decline and only a few months before we see the traditional active listing supply decline. this week we will get Male Existing home sales report, which will update that inventory data line, but total inventory levels are still historically low

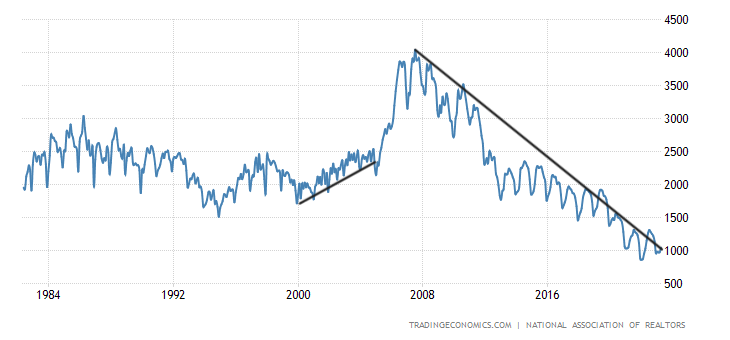

NAR Total Inventory Level,

- is among the historical list 2-2.5 million

- The peak was slightly over in 2007. 4 million

- we are currently on 1.04 million

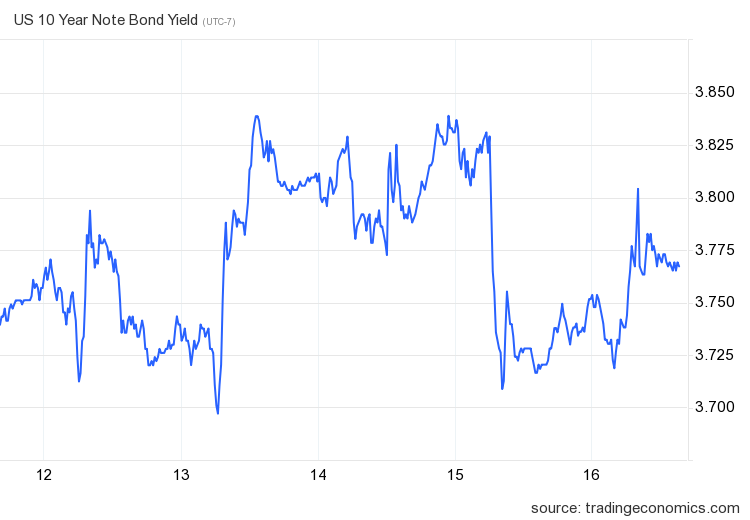

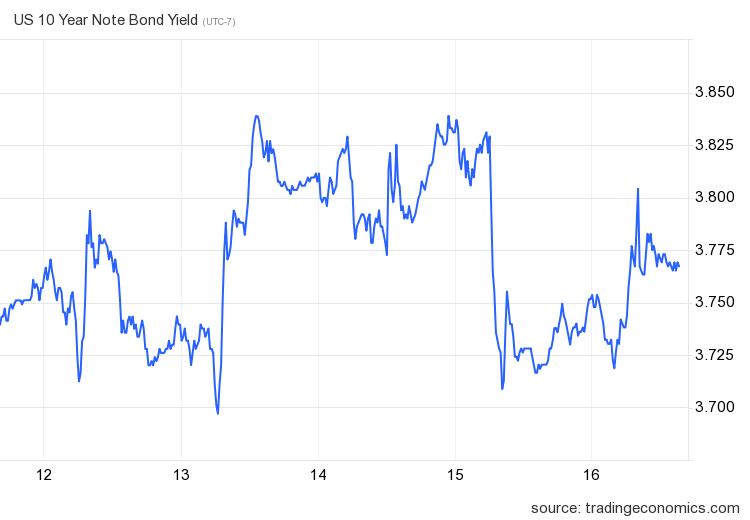

10 year yield and mortgage rates

We had a surprisingly boring week with mortgage rates, considering we also had the CPI report and the Fed meeting. Not much happened last week with mortgage rates, as they stayed in a very tight range between 6.94%-6.98%.

However, there was some exciting activity in the bond market that I should like to explain. Firstly, the bond market did not react much to the CPI report; I wrote here about the report itself, which still shows a decline in the rate of inflation growth.

However, as I’ve seen in previous weekly tracker articles, we’ve had some intriguing bond auction events since the debt ceiling action that shook the market last week. The market didn’t react much to the Fed meeting, which I talked about on this podcast. With all of those events happening last week, the chart below shows how the 10-year yield worked out.

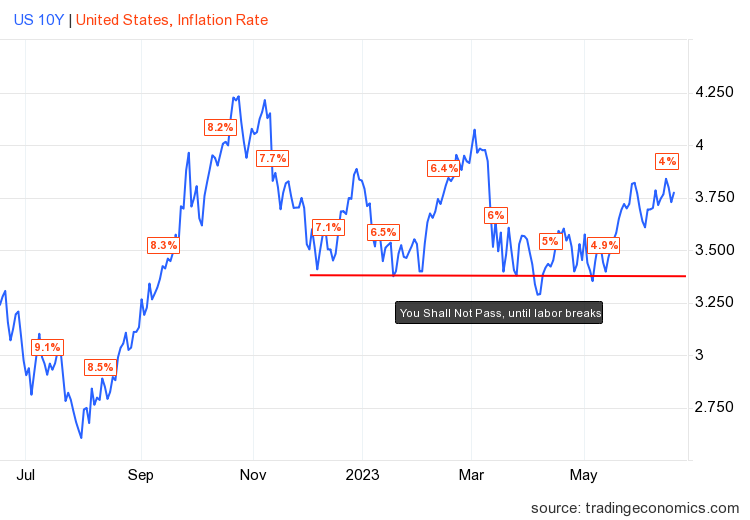

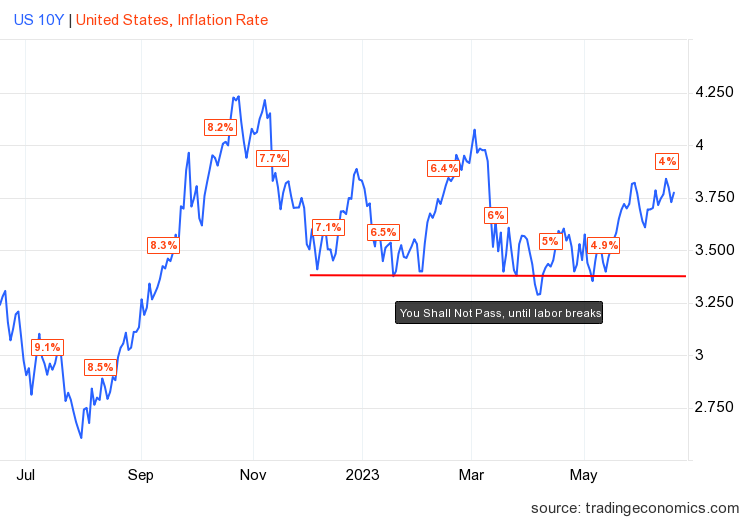

In my 2023 forecast, I wrote that if the economy remains stable, the 10-year yield range should be between 3.21% And 4.25%Equal to mortgage rates between 5.75% And 7.25%, As long as jobless claims trend below 323,000 at the four-week moving average, the labor market is stable, meaning the economy is stable.

I have also emphasized that the level between 10 years 3.37% And 3.42% It will be difficult to break down. I call it the Gandalf line in the sand: ,You shall not pass.” Yes, this may be nonsense, but I believed that breaking this level would be difficult, and Gandalf had the right line for this bond market call.

So far in 2023, that line has remained in place, as the red line in the chart below shows. mortgage rates have been in the range 5.99% -7.14%, However, we have some problems in the mortgage market.

Since the banking crisis began, the spread between the 10-year yield and 30-year fixed mortgage rates has worsened, keeping mortgage rates higher than normal. As shown below, spreads took a noticeable turn when the banking crisis drama began and have not returned to the pre-drama trend. When this data line normalizes, it will be a huge positive for the housing market. However, until then, it has been negative for the US economy.

![]()

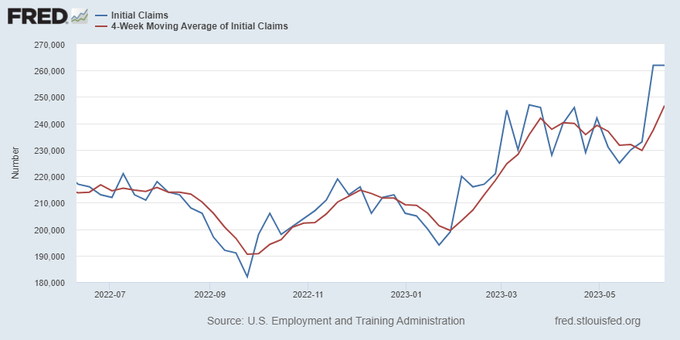

Another aspect of my 2023 forecast is that if jobless claims break down 323,000 At four-week moving average, 10-year yield could break 3.21% and towards the head 2.73%. We didn’t have much activity here last week. However, as we can see below, the labor market, while still very healthy, is not as tight as it used to be.

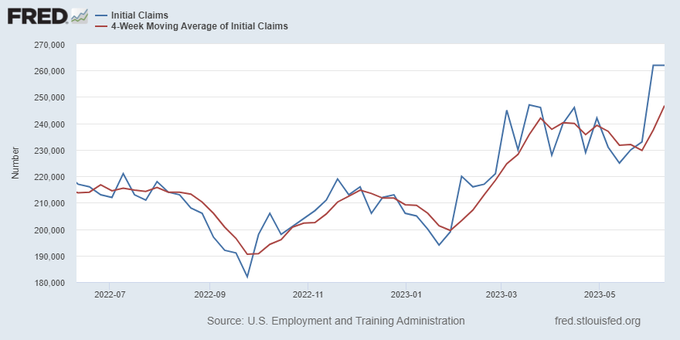

From St. Louis Fed, Initial claims for unemployment insurance benefits were little changed at 262,000 for the week ending June 10. Four-week moving average rises to 246,750

Coming Week: More Housing Data Coming!

This week we have a series of housing data being released: builder confidence, housing starts and existing home sales reports. Federal Reserve Chairman Powell will also testify to Congress this week, which could produce fireworks. Of course, I’m always on the lookout for jobless claims data to see if we can spot more cracks in the labor market.

To start with housing, we would like to see more completion of apartments as the best way to deal with inflation is always to add more supply, and we have 5 units under construction soon this is very important as without rent inflation again Increasingly, it is unlikely to ever repeat the inflation of the 1970s.

So, lets look forward to some better housing completion data this week! The best news for mortgage rates is low inflation and the best way to deal with this is more supply.