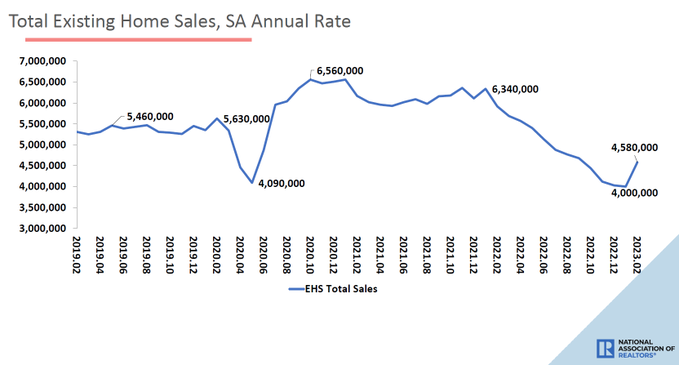

Existing home sales fell heavily short of estimates on Tuesday. This wasn’t shocking to those who follow the way I track housing data. To understand why our sales took off so quickly, you only need to go back to November 9th, when mortgage rates began to decline. 7.37% To 5.99%,

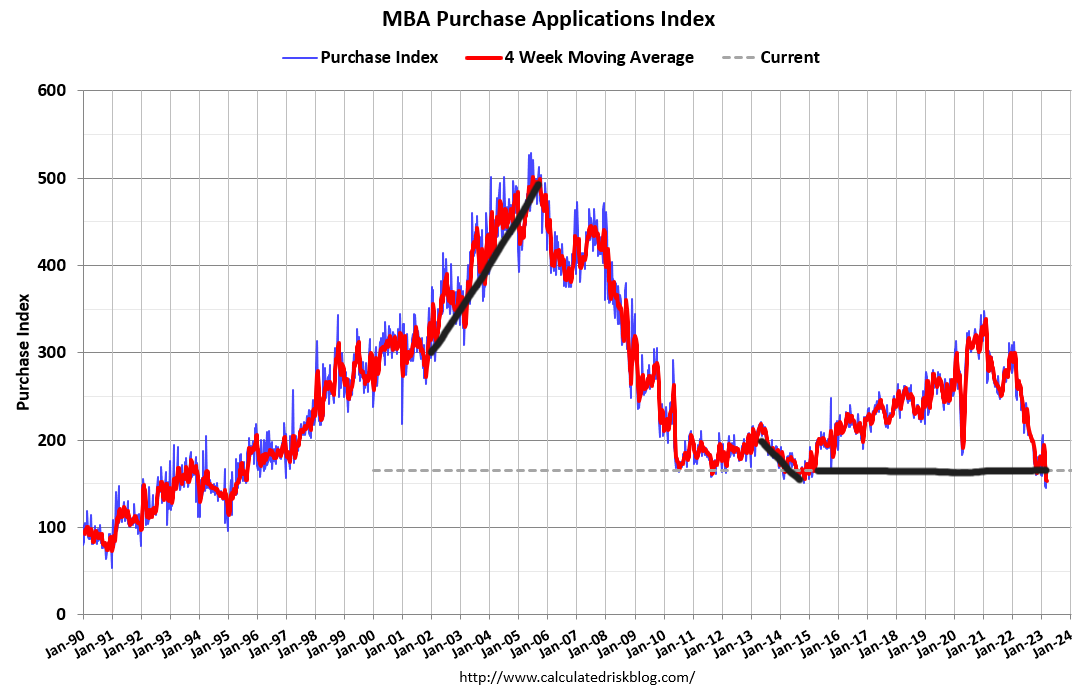

During November, December and January, the procurement application data trended positive, meaning we had several weeks of better-looking data. Weekly increases in purchase application data during those months stabilized housing sales at historically low levels.

For many years I’ve talked about how rare it is that a current home sales trend is less than 4 million. This is why the historic drop in demand in 2022 was one for the record books. We understand why sales fell during COVID-19. However, this was mainly due to behavioral change, meaning sales were poised to be higher when behavior normalised.

In 2022, it was all about affordability as mortgage rates hit historic highs. Many people didn’t want to sell their homes and wanted to move in with the very high total cost for housing, while first-time home buyers had to deal with affordability issues.

Even though mortgage rates were falling in November and December, it took 30-90 days for positive purchase application data to catch up to sales data. Therefore, as sales fell from 6.5 million to 4 million in the monthly sales data, this set a low bar for sales to grow. It’s something I talked about yesterday on CNBC, just to put the sale of this house in context of what happened before.

Because housing data and all of the economics have been so violent lately, we’ve created a weekly housing market tracker designed to look forward, not backward.

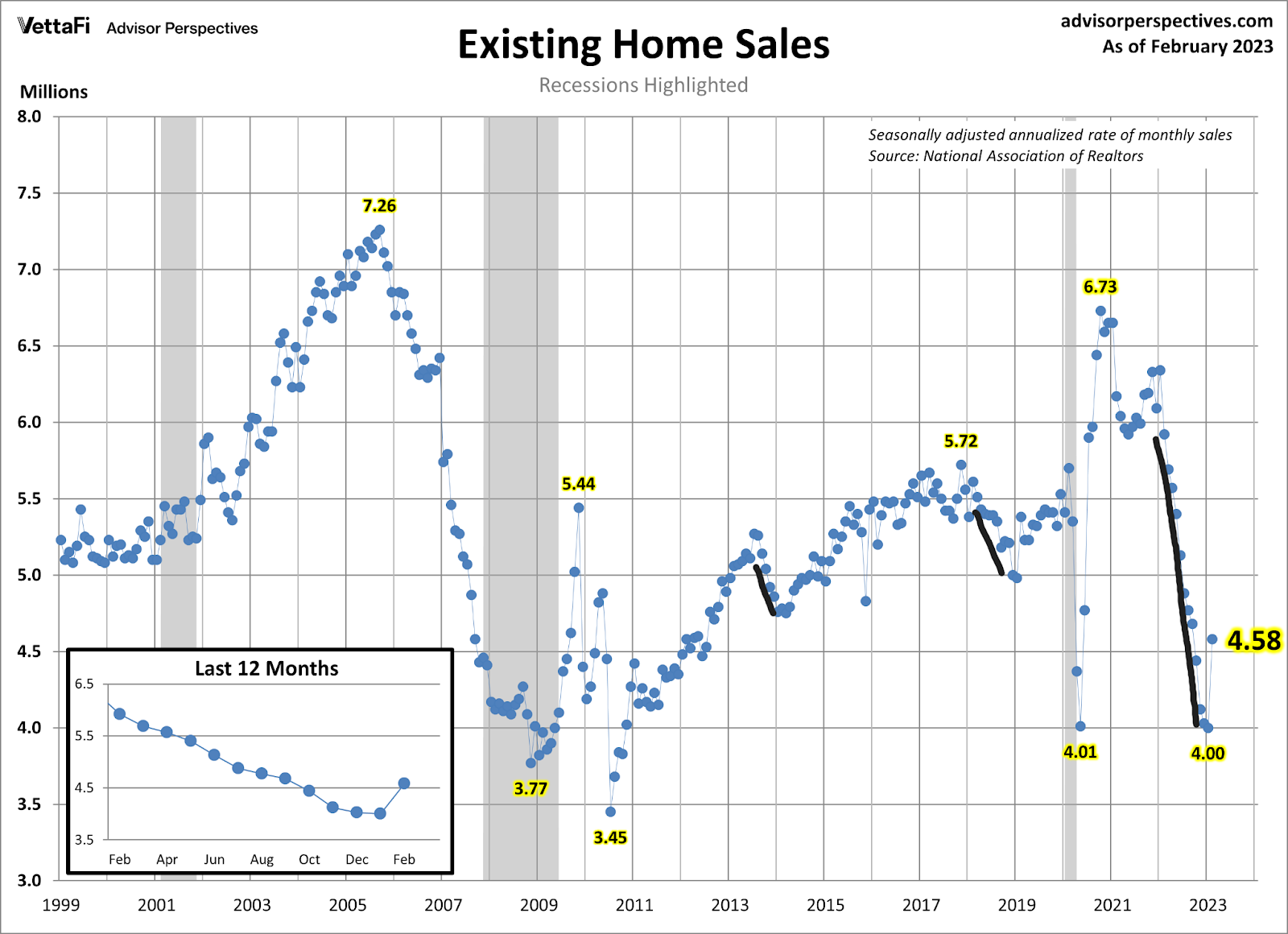

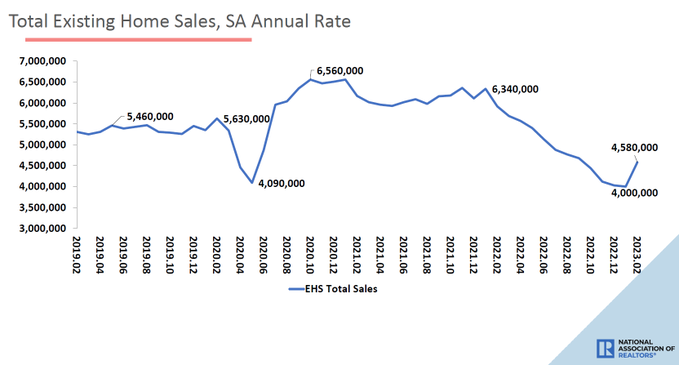

From Male, Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – rose 14.5% from January to a seasonally-adjusted annual rate of 4.58 million in February. Year-on-year, sales fell 22.6% (down from 5.92 million in February 2022).

As we can see in the chart above, the surge is very noticeable, but it stands apart from the low levels of COVID-19 and the massive rebound in sales. Mortgage rates rose from 5.99% to 7.10% this year, and that generated a month of negative forward purchase application data, which takes about 30-90 days to hit sales data.

So this report is very old and slow, but if you follow the tracker, you are not slow. This is the wild housing action I’ve talked about for a while and why Housing Market Tracker becomes helpful in understanding this data.

There was positive purchase application data over the past two weeks as mortgage rates fell from 7.10% to 6.55%; Tomorrow, we will see if we can have a third positive week. Purchases from Nov 9, 2022 One thing to remember about app data is that it has a lot more positive data than harmful data.

However, a one-month decline in purchase application data brought us back to levels seen in 1995 as recently as 1995. So, the bar is so low that we can slip.

One of the reasons the barbaric unhealthy housing market label was removed was that days on the market are now above 30 days. I am not and never will be endorsing a housing market that has days on the market in the teen years. A juvenile level means that one of two bad things is happening:

1. We have a huge credit boom in housing that will blow away with time as demand is booming similar to the run-up to the housing bubble years.

2. We don’t have enough products for homebuyers, leading to forced bidding in a low-inventory environment.

Guess which one we had after 2020? See the purchase application data above – we’ve never had a credit boom. See Inventory data below. Even with the drop in home sales and the first real comeback, total active listings are still down. 1 million.

From NAR: Total housing inventory registered at the end of February stood at 980,000 units, the same as January and up 15.3% from a year ago (850,000). Unsold inventory sits at 2.6 months of supply at the current sales pace, down 10.3% from January, but up from 1.7 months in Feb ’22. #Naresh

However, even with that, a data line that I love, love, love, days on the market, is over 30 days, and is no longer a teen like last year, when the housing market was badly hit. was unwell

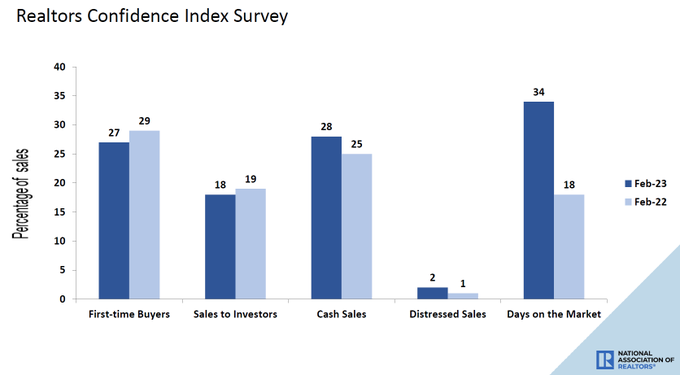

From NAR: First-time buyers accounted for 27% of sales in January; Individual investors bought 18% of the homes; All cash sales accounted for 28% of transactions; Distressed sales represented 2% of sales; Properties generally remained on the market for 34 days.

Today’s existing home sales report was good: We saw an uptick in sales as expected, and there are still more than 30 days on the market. When federal Reserve Talk about a housing reset, they’re saying they didn’t like the bidding they saw last year, so the fact that price increases don’t look like a year ago is a good thing.

Also, the market days are at a level they can feel more comfortable with. And, in this report, we didn’t see any signs of forced sales. I’ve always believed that we’ll never see the forced sales we saw during 2005-2008, which was the worst part of the housing bubble crash years. The Federal Reserve also believes this to be the case because of the better credit standards we’ve had since 2010.

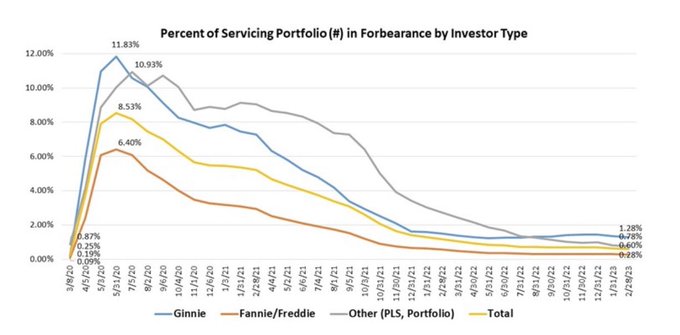

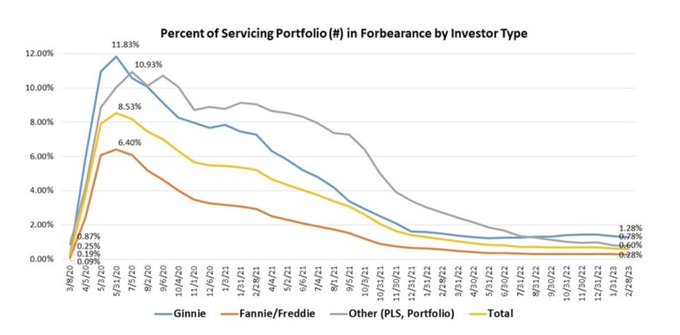

In this case, the MBA‘Recent tolerance figures show that rather than tolerance getting higher, it has collapsed. Remember, if you see a tolerance crash, bro, give them a hug, they need it.

Today’s existing home sales report looks to be lagging as purchase application data took a hit this year when mortgage rates jumped 7.10%. We can all now agree that despite the massive drop in sales, inventory data didn’t quite bode well as many have predicted for more than a decade.

I’ve emphasized that to understand the housing market, you need to understand how credit channels work post-2010. The 2005 bankruptcy reform laws and the 2010 QM laws changed the landscape of housing economics in ways that even today I don’t believe people understand.

However, the housing market took its biggest shot at affordability in 2022 and so far in 2023, and American homeowners haven’t panicked one bit. Even though this data is out of date, it shows that homeownership in America has solid ground, and just how wrong people were about the financial state of American homeownership in this country post-recession.