Not only has the data been stable, but the economic data has improved recently.

In addition, gas prices are below the peak, and inflation growth is no longer skyrocketing. If the labor market breaks this year, meaning a significant increase in jobless claims, that should send the 10-year yield 2.73%And mortgage rates can be as low as 5.25%.

Unemployment claims have been solid for some time, and that’s a big reason why I don’t believe the Federal Reserve is going to pivot out of it. He has often made it clear that he wants the labor market to collapse, so go with that premise until he says otherwise.

Housing permits will fall throughout the year, but sales have been up recently, which is positive for the economy, which means more commission transfers. An improving economy poses a higher risk of increases in rates and bond yields, especially if inflation figures rise.

If the opposite were happening, economic data would be weakened by less consumption and more people filing for unemployment claims. Rates should decline because, unlike in the 1970s, low economic growth and low jobs should not lead to high inflation, as they did in 1974.

It is true that inflation is rising at a rate we haven’t seen since the 1970s, but the reality is that if inflation in the bond market is to be believed, it is at a 10-year high over the past year. Determining the price of produce.

CPI inflation rose a few times in the 1970s along with mortgage rates and the 10-year yield. Now inflation is on the rise again, but mortgage rates have yet to top 8% as we saw in the mid-1970s, and the bond market hasn’t even broken above 5.25% at the 10-year yield. Furthermore, the Federal Reserve is not even discussing taking the fed funds rate back to late-1970s levels.

Housing was booming in the 1970s!

Have you ever wondered why the Federal Reserve said we need a housing reset in March 2022, but not a labor market reset? They are targeting the labor market in the sense that if more Americans lose their jobs, we will have a greater supply of workers, which will lead to lower wage growth and lower inflation. However, he did not use the term reset in relation to the labor market.

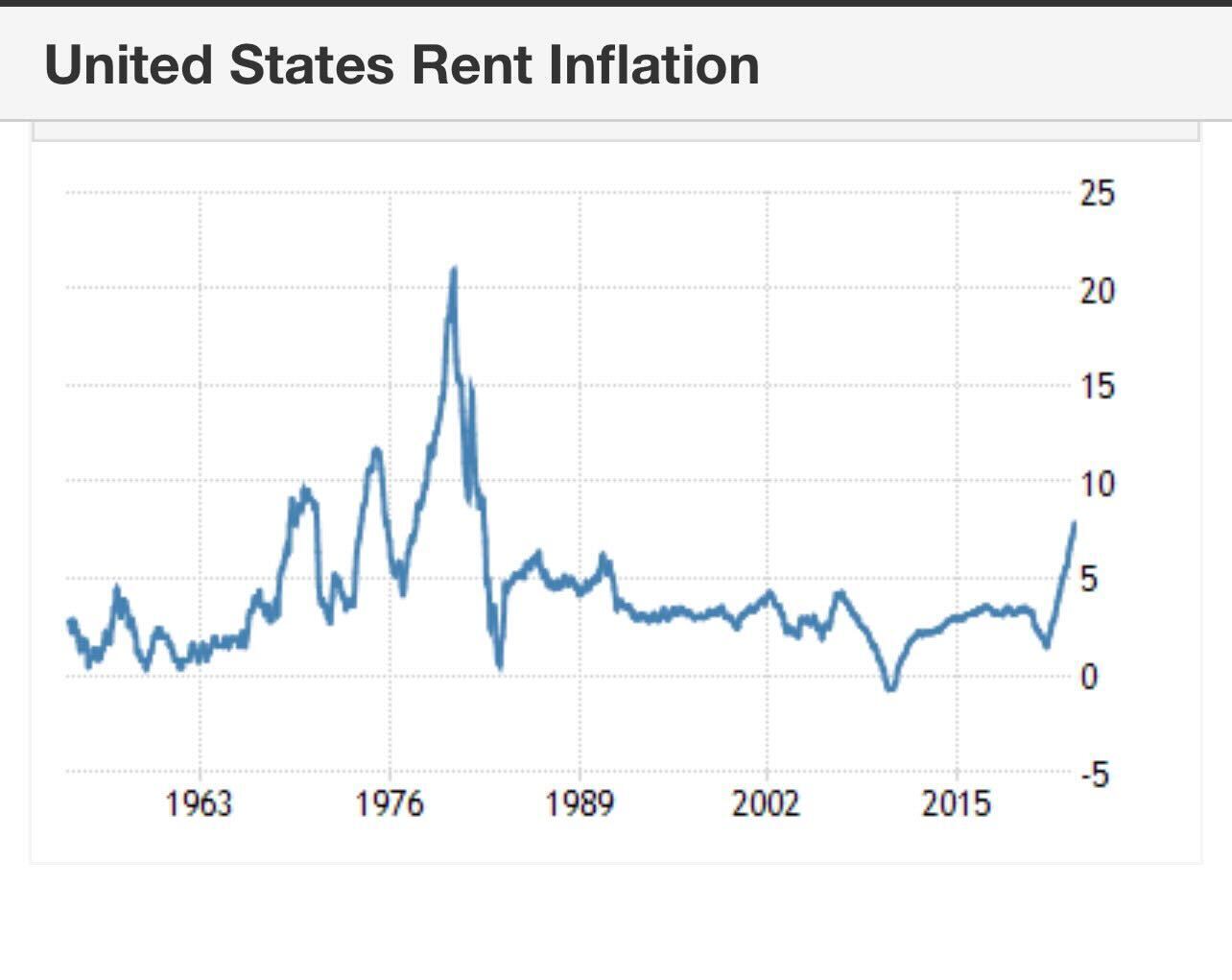

The Federal Reserve said it did not want to be stuck in the inflation of the 1970s. Which means if you believe them, they are scared to death of the housing boom! In the 1970s, we saw three booms in rent inflation, but the inflation of the mid to late 1970s is one they don’t want to see again.

Even with the recession in 1974, inflation and rates rose, and inflation and housing demand were rising more rapidly than in the late 1970s. I don’t believe they believe in this type of inflation, that’s why they’re talking about nearing the end of their rate hikes.

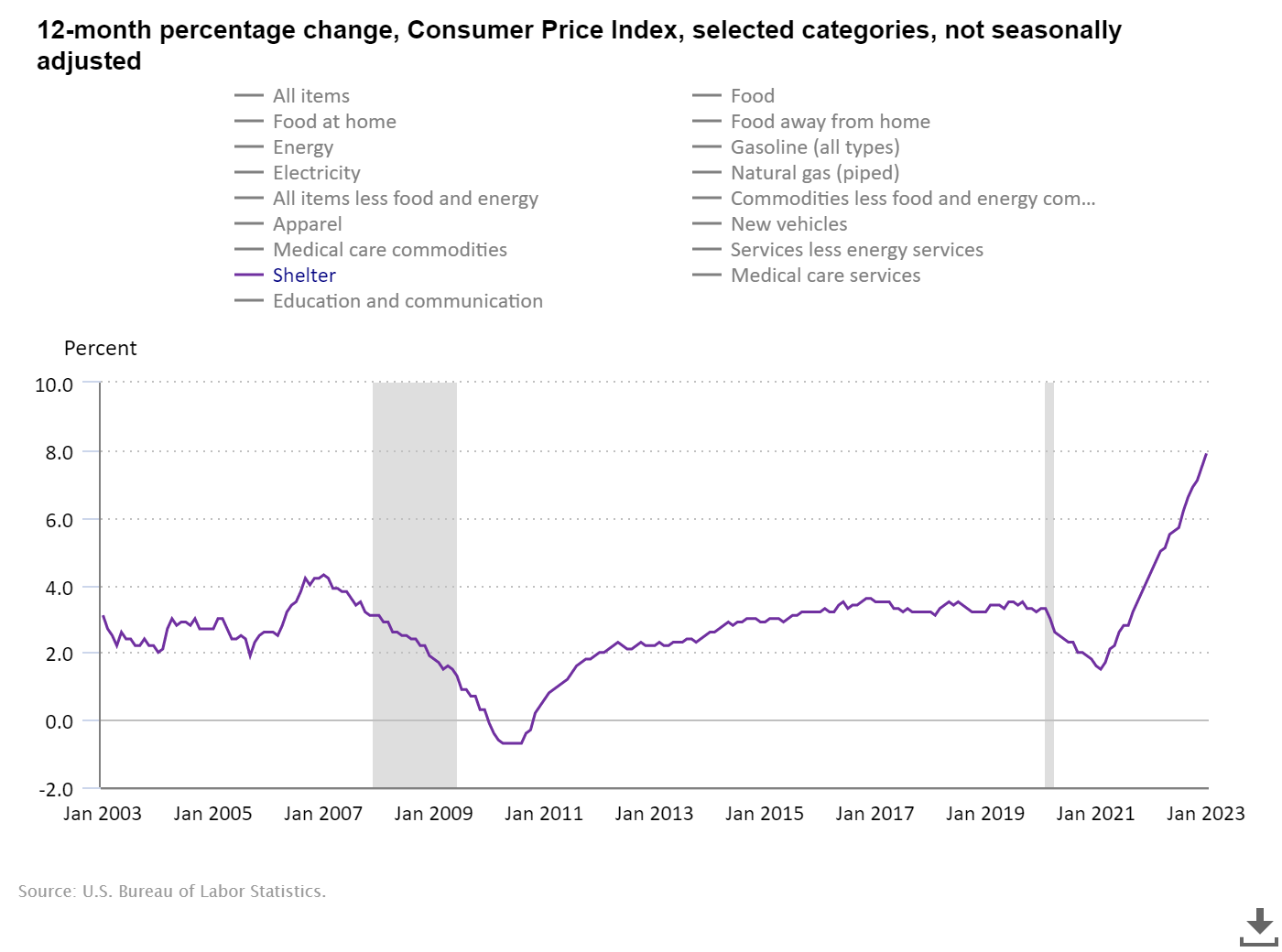

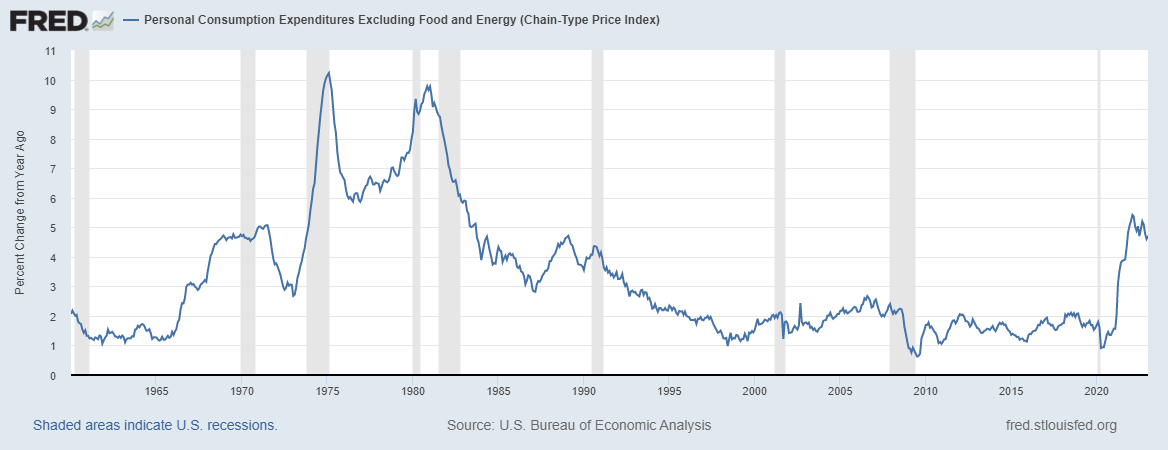

Since core CPI is sheltering inflation at 43%, you can see why rents are so important. After the 1970s, inflation growth cooled off as rent inflation calmed down and was fairly stable until the global pandemic, as you can see below, year-on-year inflation growth.

It is now well known that CPI rent inflation data is badly behind, and we are already seeing an increase in rent cooldowns, which I talked about on CNBC last September at CPI Inflation Day.

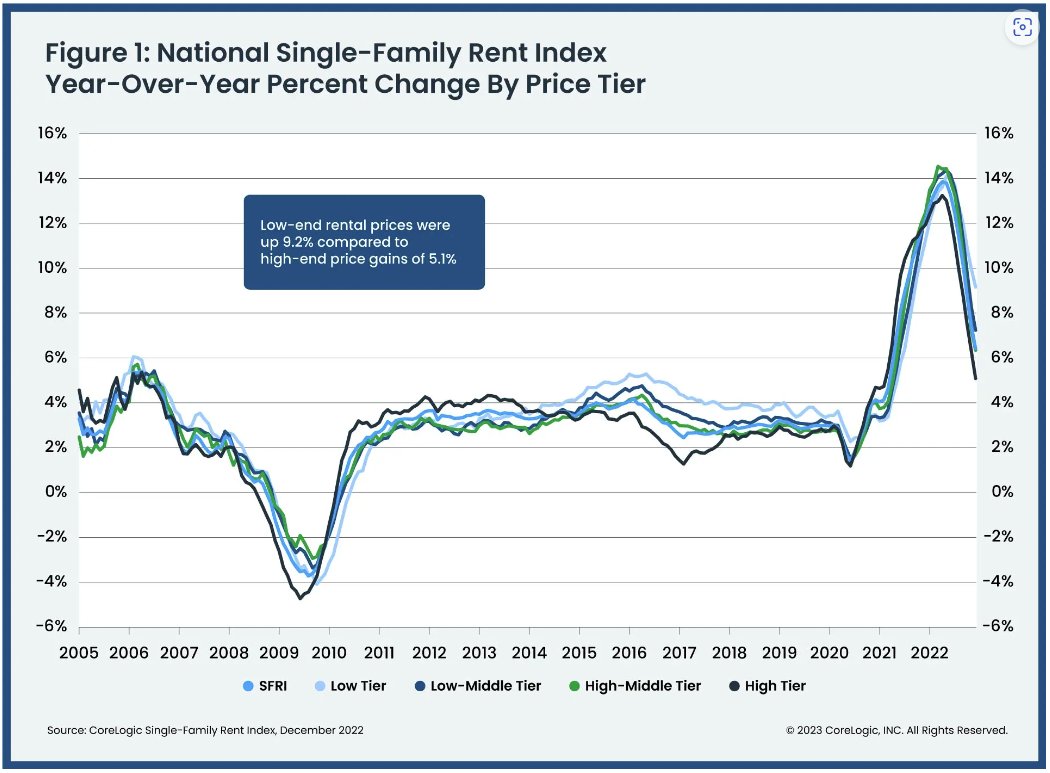

From Corelogic:

Now look at the CPI shelter inflation data today; Big difference. To the Fed’s credit, they created an inflation index to take shelter inflation out of the conversation, meaning they want to focus more on services inflation because of the lag in fare inflation.

Again, that’s why I believe they’re scared of 1970s inflation, but they also know deep down, as the bond market knows, we have a 1970s inflationary background. Not there. I wasn’t sure if they were aware of some of the time lag aspect, but they did address it in December by creating their index that doesn’t count housing inflation.

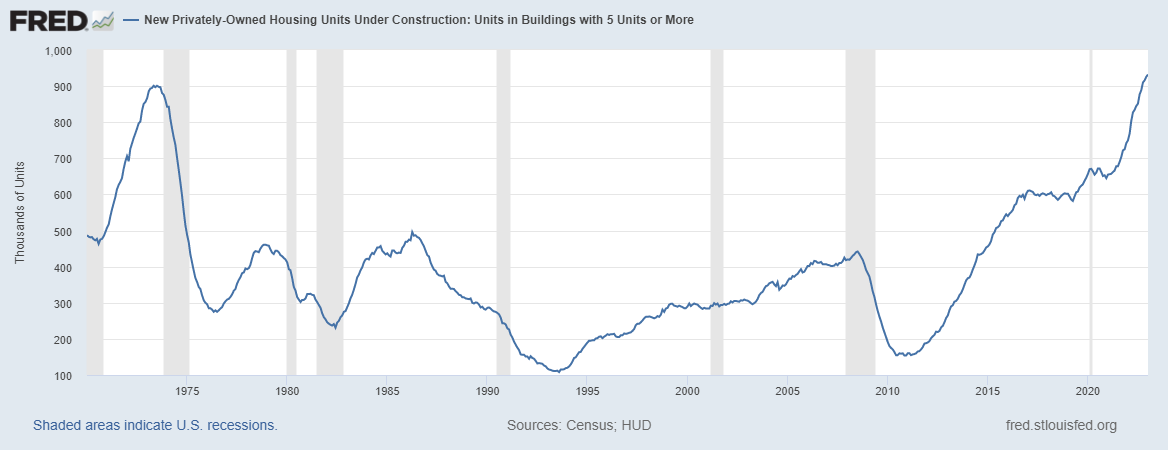

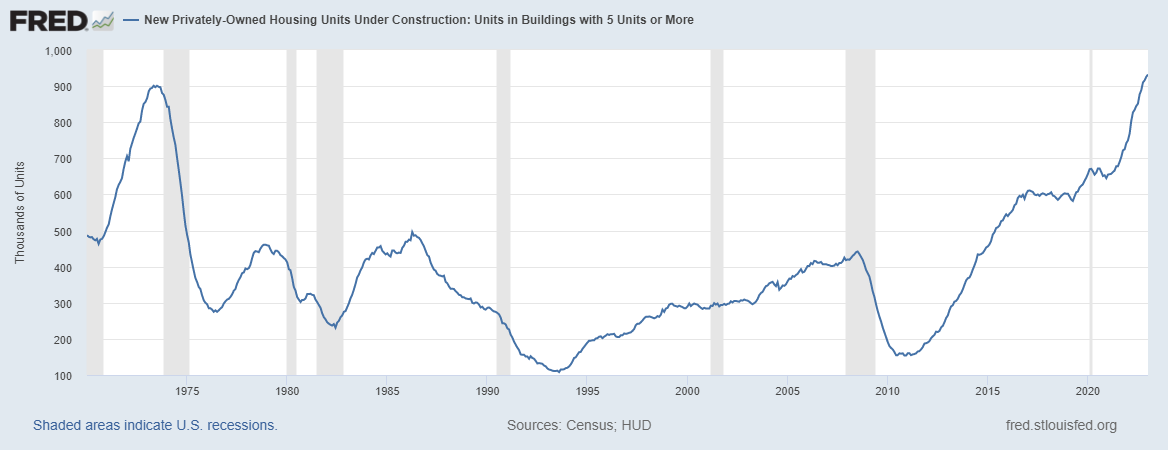

We have a record number of five-unit manufacturing underway, so the most important component of CPI is already falling in real terms. We also have good supply coming online, plus the Fed is doing what it can to cool the economy.

So the outlook here is good to contain the inflationary boom on rent growth in the 1970s. As we can see below, the recession of 1974 also killed the growth of 5 units under construction. Not so today!

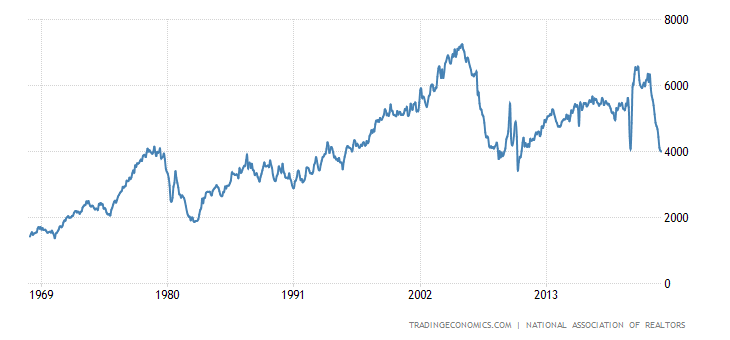

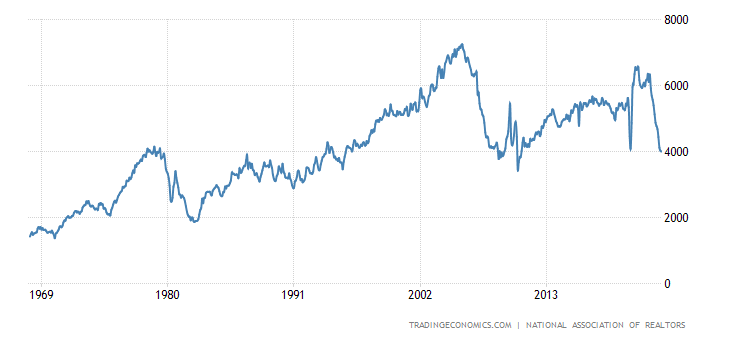

I’ve noticed recently that people don’t know how much of a housing boom happened in the mid to late 1970s. Sales of existing homes doubled before seeing a drop in demand. We went from 2 million to 4 million and back to 2 million. We are not in a bullish phase of sales demand today as existing home sales have seen the biggest drop in monthly sales in a year.

So, I’m not a Fed pivot person until jobless claims exceed 323,000 at the four-week moving average, I had a 10-year max yield 4.25% this year with a 7.25% Peak mortgage rate level. I’m not blind to the reality that the limits to inflation and growth go up as the five-unit supply line comes on.

I believe the bond market has always known this, which is why high inflation levels, 10-year yields, and mortgage rates today don’t look like they did in the 1970s.

Why would mortgage rates be less likely to rise from these levels versus more likely to fall?

Inflation growth is already coming down, supply chain is getting better, rental inflation will eventually come down to inflation figures, plus we have more supply of rental units coming on line. All these things point us towards this not being a 1970s redux.

It’s going here and there that will have a lot of economic noise and confusion, and the Fed doesn’t do themselves any favors when they talk weekly and sound like they’re confused about what to do.

At the same time, however, we should have a three-hand handle on the core PCE growth rate of inflation towards the end of the year. In the 1970s, this data line, which is the Fed’s main target level, was near 10%. Today it stands at 4.7% and even the Fed’s forecast suggests it will slow further by the end of the year.

While we’re not going to hit the Fed’s target of 2% year-over-year growth on inflation this year, core PCE growth is already slowing, which shows that the Fed and the bond market don’t trust us. Why not going to get 1970’s level inflation.

We’ve had a lot of noise about rates and inflation lately, and some say that to destroy inflation, we need a much stronger job loss recession than we expected, similar to what we saw in the 1970s. Hopefully, the data I’ve shown you today can put the 1970s to rest.

If your Baby Boomer friends are scared of the 1970s all over again, give them a hug and tell them everything will be okay; We will survive this. Don’t forget that there is a lag in Fed rate hikes, because they have a lagged effect on the economy, the Fed really wants to stop hiking sooner so they don’t have to cut rates as fast as they want.